The SEC is working hard to make good on Chairman Atkins’ promise to reduce the burdens and costs of going and staying public and facilitate access to the capital markets. On May 19, 2026, the Securities and Exchange Commission issued two proposals that would overhaul securities offerings and public company reporting. Together with the SEC’s recent proposal to permit semiannual reporting, its forthcoming proposals to reduce public company disclosure burdens and Chairman Atkins’ recent call for comments on how to modernize the IPO process, the public company landscape is undergoing a significant transformation.

The SEC’s securities offering proposal would substantially relax the requirements to be eligible to use Form S-3, widely extend the communications/registration benefits currently enjoyed by well-known seasoned issuers (“WKSIs”), permit forward and backward incorporation by reference on Form S-1, and adopt changes to the rules under the Securities Act of 1933, as amended (the “Securities Act”), to preempt state securities law registration and qualification requirements with respect to any offering registered under the Securities Act. The broad expansion would reduce the burdens of registered offerings for more issuers earlier in their public company life cycle.

The SEC’s public company filing status framework reform proposal would streamline and simplify the categories of domestic reporting issuers under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), to just two: large accelerated filers and non-accelerated filers, and extend the disclosure scaling and reporting accommodations currently available to emerging growth companies and smaller reporting companies to all non-accelerated filers. The SEC rules would create a further subcategory of “small non-accelerated filers” for those issuers with less than $35 million in assets, which would be eligible for extended reporting deadlines. Non-accelerated filers would find their public company reporting burdens significantly reduced and all filers would benefit from the ease of navigating the streamlined framework.

In light of the work the SEC is separately undertaking with respect to foreign private issuers, the SEC has not at this time extended any of these proposed changes to foreign private issuers.

The comment period for the securities offering reform proposal will close on July 27, 2026, and the comment period for the public company filing status framework reform proposal will close on July 20, 2026.

Securities Offering Changes

The SEC has long relied on criteria such as market capitalization and a minimum Exchange Act reporting history to identify whether sufficient information is available to investors outside of the four corners of a prospectus such that short form registration is appropriate. The ease of access to SEC reports enabled by technology has obviated the need for such proxies for investor access and led the SEC to focus on investor access to Exchange Act reporting.

Eligibility to Use Form S-3

The SEC’s proposal would focus Form S-3 eligibility on whether an issuer is current and timely in its public reporting. All other existing requirements for Form S-3 eligibility (including requiring one year of Exchange Act reporting history and a $75 million public float) would be eliminated. As a consequence, issuers could use Form S-3 immediately upon becoming subject to the reporting requirements of Section 13(a) or 15(d) of the Exchange Act, including for shelf offerings. To ensure investor protection in the expanded field of Form S-3 issuers, the SEC has proposed rules that would render certain issuers ineligible to use Form S-3.

Exchange Act reporting history: The SEC’s proposal would eliminate the requirement that issuers be subject to the reporting requirements of the Exchange Act for a period of 12 months. In line with the SEC’s focus on investors having access to all required information about an issuer, issuers would still need to be current and timely in their Exchange Act reporting for 12 months or such shorter period that they have been an Exchange Act reporting company to be eligible for Form S-3. The SEC has proposed a welcome grace period that would permit issuers to remain Form S-3 eligible notwithstanding an untimely filing, so long as the late filing was made within seven calendar days of its original due date (or the immediately following business day if the seventh calendar date is not a business day), and the issuer made only one untimely filing during the lookback period. Issuers relying on Rule 12b-25 would not have the benefit of an additional seven calendar days after the Rule 12b-25 deadline (but filings that comply with Rule 12b-25 would continue to be considered timely).

Other Form S-3 requirements: The proposal would otherwise delete Form S-3 requirements relating to:

- certain failures to make payments and defaults;

- all transaction requirements (including the requirement that issuers have a public float of at least $75 million and that offerings be for cash);

- electronic filing and interactive data files; and

- successor registrants (the SEC did note that successor registrants would not be tainted by tardy or delinquent filings by their predecessors and would only need to consider their own Exchange Act reporting history for the purpose of determining Form S-3 eligibility).

Form S-3 would continue to not be available for the registration of exchange offers and business combinations.

Ineligible issuers: In order to safeguard investors, the SEC’s proposal would prohibit certain issuers from using Form S-3, including issuers that are, or were in the past three years, blank check companies, shell companies (other than a business combination related shell company) and penny stock issuers, as well as issuers convicted of specified felonies or misdemeanors, or the subject to certain judicial or administrative orders or SEC proceedings. Notwithstanding the foregoing, former SPACs that are no longer shell companies would be eligible to use Form S-3.

Other prohibited issuers: Foreign governments, foreign private issuers, asset-backed issuers, investment companies and business development companies would be prohibited from using Form S-3.

Subsidiaries: Majority-owned subsidiaries that are not ineligible or otherwise prohibited as noted above, would continue to be eligible to use Form S-3 if their parent is eligible and if they are a co-registrant with their parent on the same registration statement, for the registration of fully and unconditionally guaranteed non-convertible securities (other than common equity).

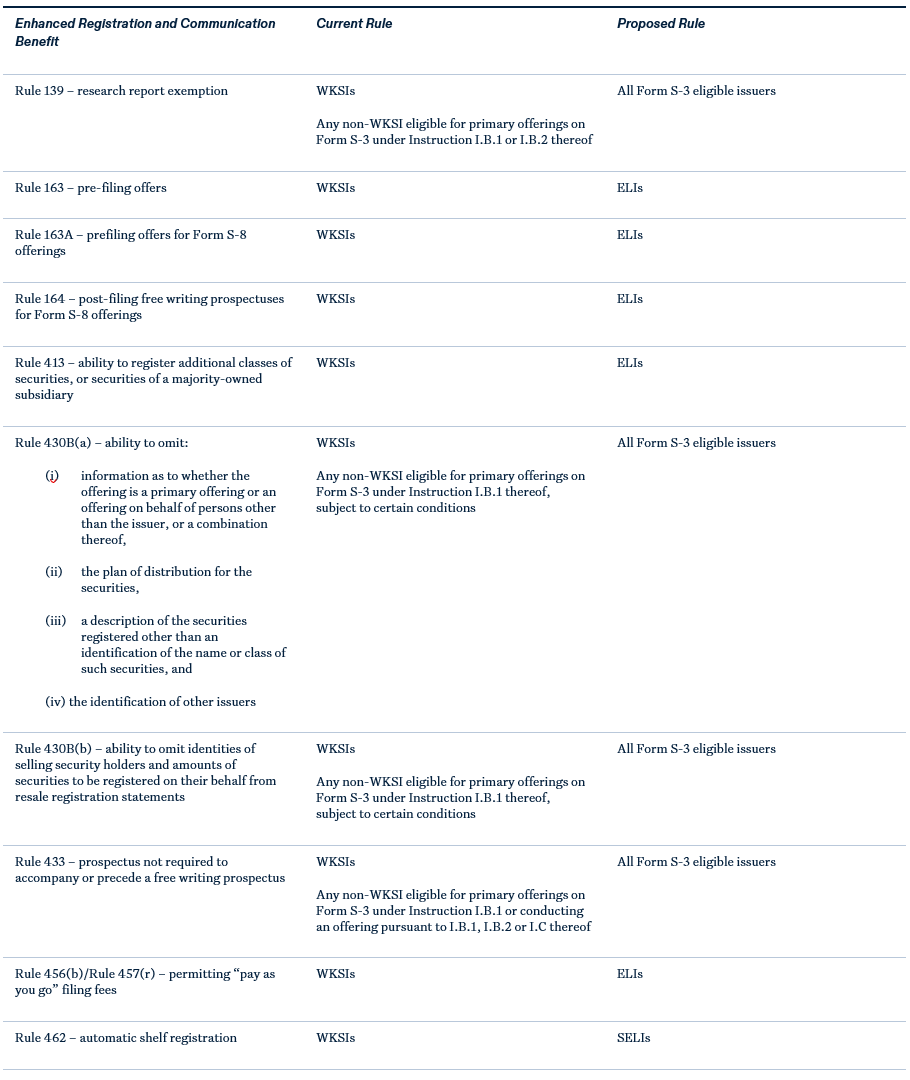

Enhanced Communication and Registration Benefits

The SEC has proposed eliminating well-known seasoned issuer (“WKSI”) status for domestic issuers and replacing it instead with two categories of issuers:

- Eligible Listed Issuers (“ELIs”) – issuers eligible for Form S-3 who have a class of common equity securities listed on a national securities exchange; and

- Seasoned Eligible Listed Issuers (“SELIs”) – ELIs who have been subject to the Exchange Act’s reporting requirements for a period of at least 12 full calendar months preceding the relevant measurement date. Successor issuers (other than former SPACs) would be able to rely on the Exchange Act reporting history of their predecessors for purposes of determining whether the successor satisfies the 12-calendar month seasoning requirement. Former SPACs would not be able to rely on their predecessor’s reporting history for the purposes of meeting SELI eligibility.

Neither ELI nor SELI status would retain a public float/registered debt issuance requirement, vastly expanding the issuer pool eligible to use these rules. In its proposing release, the SEC noted that in 2024, approximately 36% of Exchange Act reporting issuers were WKSIs; by contrast, 74% of Exchange Act reporting issuers in 2024 would have qualified as SELIs. The SEC would retain the WKSI definition for foreign private issuers, and is not proposing extending these amendments to foreign private issuers at this time. Like WKSI status, ELI and SELI status would be measured once a year.[1]

ELIs would be eligible to use the enhanced communication and registration benefits currently afforded to WKSIs, except for automatically effective registration statements – only SELIs would be eligible to file automatically effective registration statements. Consistent with current rules which permit non-WKSIs eligible to use Form S-3 for primary offerings to use Rules 139 (research report exemption), 430B (permitting the omission of certain disclosure from the registration statement) and 433 (not requiring a prospectus to accompany or precede a free writing prospectus), Form S-3 eligible issuers would be eligible to rely on Rules 139, 430B and 433 as well. See Annex A for more details.

Subsidiaries: Majority-owned subsidiaries using Form S-3 as described above would be eligible to be treated as an ELI or SELI, according to the status of the parent.

Incorporation by Reference on Form S-1

Those few issuers[2] still using Form S-1 after the SEC’s proposed amendments become effective that are subject to, and have been current in their, Exchange Act reporting (though they need not have been timely) would be freely able to incorporate by reference into their registration statements on Form S-1, both backwards and forwards, their Exchange Act reports and any Securities Act registration statement filing (if no Form 10-K is yet filed). Issuers that are or were in the prior three years blank check companies, shell companies and penny stock issuers would not be eligible to incorporate by reference, nor would issuers registering an offering that effects a business combination on the Form S-1. Notwithstanding the foregoing, former SPACs would be eligible to incorporate by reference on Form S-1.

The categories of issuers ineligible to use Form S-1 would be expanded: currently foreign governments and asset-backed issuers are ineligible to use Form S-1; under the proposed rules, foreign private issuers, investment companies and business development companies would also be ineligible.

At the Market Offerings

In light of the expanded access to Form S-3 and shelf offerings, the SEC has proposed amending Securities Act Rule 415(a)(4) to restrict at-the-market (“ATM”) offerings to just those securities that are listed or traded only on a national securities exchange, or in a market designated by the Commission (currently, Rule 415(a)(4) only requires that the securities be sold into “an existing trading market” for the outstanding securities).

Pre-emption of State Securities Laws

To reduce the burdens of blue sky compliance and facilitate capital formation, the SEC has proposed technical amendments to Securities Act rules that would exempt all securities offering under Securities Act registration statements from state securities laws.

Public Company Filing Status and Reporting Changes

The many efforts the SEC and Congress have undertaken over the last quarter century to reduce burdens for various issuers to access the public markets and reduce reporting burdens have resulted in several complicated sets of sometime overlapping filing statuses and varied reporting obligations. The SEC has proposed simplifying this framework and extending the scaled disclosure and reporting requirements to reduce regulatory burdens and encourage more companies to go and stay public.

Large Accelerated Filers

Under the SEC’s proposal, issuers that meet the following public float and reporting history requirements would be considered large accelerated filers:

Public float: A public float held by non-affiliates of $2 billion (up from the current $700 million), calculated based on the average stock price over the last 10 trading days of the second fiscal quarter, or first six-month fiscal period if semiannual reporting is adopted (extended from the current measurement of market capitalization as of the last day of the second fiscal quarter, to mitigate the impact of a single trading day’s volatility on the determination), in each of the last two fiscal years (up from just the most recent fiscal year, to ensure relative stability of the issuer’s status, as well as to provide early visibility into the possibility of a status transition). Because of the heightened thresholds to be met, the SEC has proposed the same standard for measuring both when an issuer would become a large accelerated filer as well as when an issuer would lose its status as such.

Public reporting: 60 consecutive calendar months of reporting (up from a year to allow companies additional time to adjust to being public before needing to comply with the full complement of requirements applicable to large accelerated filers). The SEC has requested comment on whether it would be appropriate to shorten this period for especially large public companies for whom the burden of public reporting as a large accelerated filer should be mitigated by their resources.

According to the SEC’s estimates, 19.2% of existing Exchange Act reporting companies would be large accelerated filers under the proposed rules, representing approximately 93.5% of total market public float.

The filing obligations of large accelerated filers would be unchanged.

Non-accelerated Filers

All issuers that are not large accelerated filers would be non-accelerated filers, eligible for the following scaled disclosure/reporting accommodations:

- extended deadlines for periodic report filings (90 days for Annual Reports on Form 10-K; 45 days for Quarterly Reports on Form 10-Q);

- no need to provide an auditor attestation report pursuant to Item 308(b) of Regulation S-K;

- prepare financial statements in accordance with Article 8 of Regulation S-X, including the reduced financial statement requirements thereof:

- two years of audited statements of comprehensive income, cash flows and changes in stockholders’ equity (instead of three);

- more condensed format for interim financial statements, financial statements for businesses and real estate operations acquired or to be acquired and pro forma financial statements;

- reduced description of business (notably, segment disclosure would not be required and human capital resources disclosure would be limited to the number of employees) per Item 101(a) of Regulation S-K;

- two years of MD&A (instead of three) per Item 303 of Regulation S-K;

- reduced executive compensation disclosures:

- two years of summary compensation table information (instead of three) per Item 402 of Regulation S-K;

- executive compensation disclosures regarding three named executive officers (instead of five) per Item 402 of Regulation S-K;

- no need to provide: compensation discussion and analysis, compensation policies and practices related to risk management, pay ratio disclosure, pay vs performance disclosure and specific executive compensation disclosure tables (grants of plan-based awards, pension benefits, option exercises and stock vested table and nonqualified deferred comp) pursuant to Item 402 of Regulation S-K, or compensation committee interlocks and insider participation disclosure or Compensation Committee Report disclosure pursuant to Item 407 of Regulation S-K;

- no need to hold “say on pay,” “say on frequency of pay” or “say on golden parachute” votes;

- no need to provide:

- risk factor disclosure in Forms 10-K and 10-Q (though issuers may find good reason to continue this practice and risk factor disclosure remains a registration statement requirement);

- performance graph disclosure comparing stock performance to peers per Item 201(e) of Regulation S-K;

- supplementary financial information reflecting retrospective material changes to the financial statements pursuant to Item 302(a) of Regulation S-K;

- quantitative and qualitative disclosures about market risk pursuant to Item 305 of Regulation S-K;

- policies and procedures for the review, approval or ratification of related party transactions per Item 404(b) of Regulation S-K;

- audit committee financial expert disclosure in the first annual report;

- certain payments made by resource extraction issuers pursuant to Rule 13q-1 under the Exchange Act.

Foreign Private Issuers and SPACs

As noted above, the SEC has deliberately excluded foreign private issuers from these proposed offering and filer status rule changes. Under the proposed rules, foreign private issuers would be ineligible to use Forms S-3 and S-1 (and thus could not take advantage of the offering reforms by filing on domestic forms instead of Forms F-3 and F-1), and would be ineligible for the expansion of the scaled disclosure requirements and reporting accommodations available to non-accelerated filers.

While shell companies would not enjoy the benefits of the securities offering reforms, as noted above, the SEC has very specifically provided that former SPACs would be eligible to do so.

Conclusion

Together, these proposed rule changes would vastly reduce reporting and registration burdens for many public companies, especially newly public companies. If the rules are adopted as proposed, upon completing its IPO, an issuer would have significantly reduced reporting obligations for the first five years, and the benefit of certainty about its reporting obligations for that five-year period. At the same time, that newly public issuer would have immediate access to Form S-3 (including incorporation by reference and shelf offerings) and the benefits of enhanced communications currently accessible only by WKSIs, and, after a year of timely reporting, access to automatic shelf registration statements, all of which would greatly facilitate access to capital markets. For companies debating the costs of going or staying public, these reforms could be very persuasive.

Annex A – Enhanced Communication and Registration Benefits Available to WKSIs

|

* * *

[1] ELI/SELI status would be measured as of the latest of: the date the issuer files a registration statement on Form S-3, the date of its section 10(a)(3) amendment to its Form S-3 (or such due date), or if the issuer has not filed or amended a registration statement to comply with section 10(a)(3) of the Securities Act for 16 months, the date of filing its most recent annual report on Form 10-K.

[2] Issuers that have not been timely in their reports during the lookback period and issuers ineligible to use Form S-3 (blank check companies, shell companies, penny stock issuers as well as issuers convicted of specified felonies or misdemeanors, or subject to certain judicial or administrative orders or SEC proceedings).