On 12 March 2026, the UK government published its planned changes to the 17 (now 19) sensitive sectors for mandatory and suspensory notification for qualifying transactions under the National Security and Investment Act 2021 (the “NSIA”). Notification is required for the acquisition of shares or voting rights that crosses the threshold of more than 25%, more than 50% or 75% or more, in a qualifying entity that carries on activities in one of the relevant sensitive sectors in the UK, or where the acquirer obtains the right to pass or block any class of resolution governing the affairs of the qualifying entity.

The announcement follows on from last summer’s consultation (discussed in our client memo).

In summary

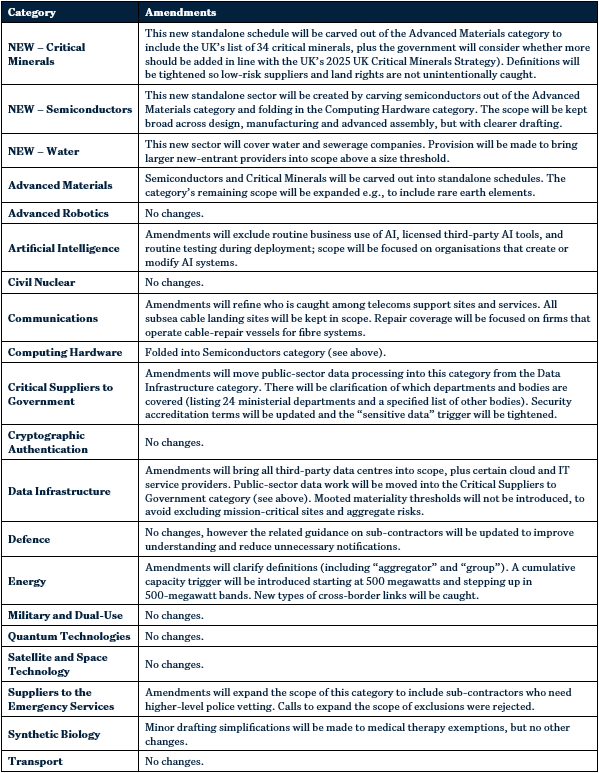

- Water will be added as a new mandatory sector;

- Semiconductors will be carved out of the Advanced Materials category to become a standalone sector, and the current Computing Hardware category will be folded into it;

- Critical Minerals will also be carved out of the Advanced Materials category to become a standalone sector;

- The Artificial Intelligence category will be amended to reduce its scope and a number of other categories will see amendments to improve clarity; and

- Updated and more detailed guidance will be issued to reflect the above changes and address points raised in the consultation. The changes will clarify scope, provide worked examples, and support assessment of whether a transaction falls within the mandatory notification regime.

Points to note

- These changes will be made by secondary legislation, to be published later this year.

- They are not expected to reduce notifications: the government estimates that they will generate a slight increase of around 10 extra notifications per year. In the last annual report on the NSIA, the UK government reported 1,143 notifications during the 12 months to end March 2025 (up 26% on the prior year) – one of the highest levels of investment screening filings globally.

- Notifications are predicted to reduce for the AI and Communications sectors, but to increase for Data Infrastructure, Emergency Services Suppliers and Critical Minerals (without any reduction in notifications in the Advanced Materials sector that Critical Minerals were carved out of).

- The UK government has recently rejected calls from a parliamentary committee to streamline the NSIA regime, including introduction of a fast track for accredited “allied” capital (see our client memo). The government countered that around 95% of notifications are cleared within 30 working days, and noting that national security risk is not only linked to the acquirer but can also flow from the target, or the level of control.

- This blind spot to the burden of the NSIA regime on investors stands in stark contrast to UK merger control, where government pressure on the Competition and Markets Authority to be pro-growth and pro-investment has resulted in a significant drop in intervention rates, with Phase 2 referrals in 2025 around half the level of previous years and no (new) prohibitions for the first time since 2017.

- There is no discussion in the consultation response of the separate NSIA reforms announced last summer to remove internal reorganisations and insolvency-related appointments from its scope. Legislation to create these new exemptions (which should have a positive impact, reducing notifications) is still awaited.

- The EU institutions are currently finalising the revised FDI screening regulation (discussed in our client memo) which will conform a minimum baseline for the sectors for mandatory scrutiny under Member States’ FDI regimes. The revised UK regime will be broader in some respects (including Advanced Robotics, Critical Suppliers to Government and Synthetic Biology) and narrower in others (EU Member States must include electoral infrastructure and certain financial markets infrastructure and systemically important entities).

- Separately, the EU Commission’s Industrial Accelerator Act proposes a new layer of pan-EU FDI controls and conditions on investors into certain strategic sectors from ex-EU countries with more than 40% of global manufacturing capacity for the sector concerned. These proposals are focused on boosting EU industrial capacity in strategic sectors rather than on national security. They are controversial and at an early stage of the legislative process, so may change (see our client memo for more).

- It remains the case that FDI scrutiny is ever-growing, with geopolitics making the assessment of national and economic security more complex. Dealmakers should build FDI review and clearance into deal strategy, planning and timings from the outset.

Revisions to the mandatory sectors

|

* * *