The SEC has reopened the comment period for its 2015 pay for performance proposal. Interested parties are called upon to provide input on the SEC’s initial proposal (available here) and additional questions posed by the SEC in its release reopening the comment period (available here). The proposal would implement Section 14(i) of the Securities Exchange Act of 1934 (the “Exchange Act”), as added by Section 953(a) of the Dodd-Frank Act. Section 14(i) directs the Commission to adopt rules requiring reporting companies to disclose in a clear manner the relationship between executive compensation actually paid and the financial performance of the company.

Under the proposal, reporting companies would be required to disclose in their proxy and information statements standardized figures for compensation “actually paid” to the principal executive officer, the average compensation “actually paid” to the remaining named executive officers, and certain performances measures, including the company’s total shareholder return and total shareholder return for a peer group of companies and the relationship between the performance measures and compensation. Disclosure would be required for the last five fiscal years subject to a transition period. These requirements would apply to all reporting companies, except foreign private issuers, registered investment companies and emerging growth companies. Smaller reporting companies would be subject to scaled reporting requirements.

The comment period will be open for 30 calendar days after publication of the release in the Federal Register.

Proposed Tabular Disclosure

Under the initial proposal, proposed new Item 402(v) of Regulation S-K would require companies to disclose, in any proxy or consent solicitation material for an annual meeting of shareholders, in tabular format for each of the last five fiscal years:

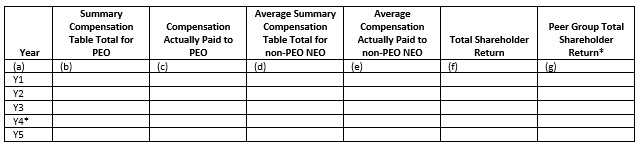

- total compensation paid (as currently required for the Summary Compensation Table), and a new figure of compensation “actually paid,” to the principal executive officer (as defined in Item 402(a)(3) of Regulation S-K, (“PEO”)). If more than one person served as PEO during any covered period, then the compensation for all PEOs will be aggregated for those years;

- average total compensation paid (as derived from the current Summary Compensation Table), and a new figure of average compensation “actually paid,” to the other named executive officers (as defined in Item 402(a)(3) of Regulation S‑K, (“NEOs”));

- total shareholder return (“TSR”) of the company, as measured by dividing the sum of the cumulative amount of dividends for the measurement period, assuming dividend reinvestment, and the difference between the company’s share price at the end and the beginning of the measurement period, by the share price at the beginning of the measurement period (as set forth in Item 201(e) of Regulation S-K); and

- TSR of a peer group.

An example of the tabular disclosure called for by proposed Item 402(v) is set forth below:

The SEC is now considering whether to also require the following additional measures be included in the tabular disclosure:

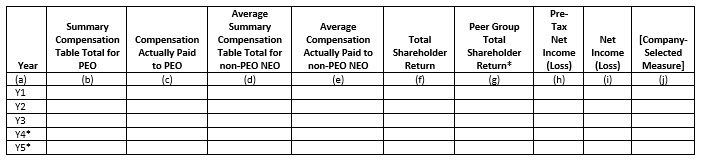

- pre-tax net income (loss),

- net income (loss), and

- the measure most important to the company’s compensation determinations (the “company selected measure”).

An example of the tabular disclosure including these additional measures is set forth below:

In addition, the SEC is now considering whether to require companies to identify and rank the five performance measures they use most to link compensation actually paid during the fiscal year to company performance. If a company uses fewer than five such measures it would only need to disclose the measures it actually uses. The SEC is considering requiring this additional disclosure be presented in tabular format as well.

Although the Summary Compensation Table and accompanying tables currently required under Item 402 of Regulation S-K are subject to detailed rules with respect to various elements of executive compensation, there is no requirement for tabular disclosure containing a uniform metric permitting an evaluation of executive compensation relative to the company’s financial performance. By contrast, the proposed pay-for-performance rules would create uniform standards for calculating actual compensation paid to a company’s PEO and other named executive officers, as well as a uniform metric for assessing compensation relative to financial performance. Essentially, this means that subject companies will need to assemble in one location certain already-disclosed elements of executive compensation (e.g., total compensation paid, TSR) and calculate additional elements (e.g., compensation “actually paid,” as described below).

Determination of Compensation “Actually Paid”

Under proposed Item 402(v), compensation “actually paid” derives from the total compensation currently reported in the Summary Compensation Table, adjusted to reflect certain pension benefit and equity award changes by:

- deducting the aggregate change in the actuarial present value of all defined benefit and actuarial pension plans reported in the Summary Compensation Table;

- adding the service cost under all defined benefit and actuarial pension plans, consistent with “service cost” as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 715;

- deducting the fair value of stock and option awards at grant date (i.e., the amounts reported pursuant to Items 402(c)(2)(v) and (vi)); and

- adding the fair value of stock and option awards (with or without stock appreciation rights) at vesting date, computed in accordance with fair value guidance in FASB ASC Topic 718.

A company would be required to include footnotes to the pay versus performance table explaining the amounts deducted from and added to the total compensation reported in the Summary Compensation Table pursuant to the adjustments described above, together with the vesting date valuation assumptions used by the company (if materially different from the grant date assumptions disclosed in its financial statements).

The SEC noted that some companies have used “realizable” or “realized” pay or other pay or performance concepts in their disclosure, and may continue to do so as a supplement to the new Item 402(v) requirements so long as those other figures are not misleading and not presented more prominently.

Peer Group

The peer group used for purposes of the proposed Item 402(v) disclosure should be the same as the peer group used in the company’s Form 10-K performance graph disclosure (Item 201(e)(1)(ii) of Regulation S-K) or the peer group used in the Compensation Discussion & Analysis (“CD&A”) of its proxy statement (Item 402(b)(2)(xiv) of Regulation S-K). If the peer group is not a published index, the company would be required to disclose the identity of the issuers. If the company has previously disclosed the composition of such peer issuers in prior filings, the company may comply with the proposed disclosure requirement by incorporation by reference to those filings.

Time Period Covered

Companies would be required to provide disclosure for the five most recently completed fiscal years that it was a reporting company pursuant to Section 13(a) or Section 15(d) of the Exchange Act. The proposed rules includes a transition period, however, such that in the first applicable filing after the proposed rules become effective, companies would be required to provide disclosure for only the three most recently completed fiscal years, and then provide disclosure for an additional year in each of the two subsequent annual proxy filings where disclosure is required.

Proposed Comparative Disclosure

In addition to the foregoing tabular disclosure, the company would be required to provide a (i) description of the relationship between the executive compensation actually paid and the company’s TSR and (ii) comparison of the company and peer group TSR, in each case for the last five years. This disclosure could be made in narrative form, graphically (for example, by means of a graph providing executive compensation actually paid and change in TSR on parallel axes and plotting compensation and TSR over the required time period), or through a combination of both.

Other Provisions

The SEC did not specify a location for the new disclosure items. Some companies may wish to include these items in the CD&A, but the SEC noted that including this information in this manner would suggest that the company considered the pay-for-performance relationship (as disclosed) in its compensation decisions, which may or may not be the case.

The proposed Item 402(v) disclosure would not be deemed to be incorporated by reference into any other SEC filing, unless the company specifically states otherwise. However, because the disclosure is required pursuant to Item 402 of Regulation S-K, it may be required to be included in certain registration statements under the Securities Act and the Exchange Act, and also in annual reports on Form 10-K to the extent that Item 402 disclosure is required. Further, Item 402(v) would be subject to the say-on-pay advisory vote of shareholders.

Finally, the SEC will require the new disclosure to be tagged using XBRL formats.

* * *

Related Insights