The following is our summary of significant U.S. legal and regulatory developments during the first quarter of 2026 of interest to Canadian companies and their advisors.

SEC Adopts Final Rules to Implement Section 16 Reporting by Directors and Officers of Foreign Private Issuers and Issues Order Exempting Insiders of Certain Foreign Private Issuers from Section 16 Reporting

On February 27, 2026, the Securities and Exchange Commission (the “SEC”) adopted final rules implementing the Holding Foreign Insiders Accountable Act. The Holding Foreign Insiders Accountable Act was signed into law on December 18, 2025, and amended Section 16(a) of the Securities Exchange Act of 1934 (the “Exchange Act”) to extend Section 16 reporting obligations to directors and officers of foreign private issuers. The rules adopted by the SEC make technical amendments to Rule 3a12-3(b) under the Exchange Act and Forms 3, 4 and 5 to implement the reporting by directors and officers of foreign private issuers pursuant to Section 16(a), as required by, and consistent with, the Holding Foreign Insiders Accountable Act.

On March 5, 2026, the SEC issued an order exempting directors and officers of certain foreign private issuers from the reporting requirements of Section 16(a) of the Exchange Act, as extended by the Holding Foreign Insiders Accountable Act. The exemption from reporting is available for directors and officers of foreign private issuers incorporated or organized in a qualifying jurisdiction who are subject to the qualifying regulations (requiring reporting of securities transactions by insiders) of any of those qualifying jurisdictions. Canada is a qualifying jurisdiction and National Instrument 55-104 – Insider Reporting Requirements and Exemptions (supported by National Instrument 55-102 – System for Electronic Disclosure by Insiders (SEDI) and companion policies) is a qualifying regulation. In its exemptive order, the Commission noted that any director or officer seeking to rely on the exemption (1) must report their transactions in the issuer’s securities as set forth under the qualifying regulation and (2) if such report is not in English, it must be made available in English to the general public within no more than two business days of its public posting (publishing it on the issuer’s website is sufficient).

The final rules became effective on March 18, 2026.

For the full text of our memorandum concerning the adoption of the final rules, please see:

For the full text of our memorandum concerning the SEC’s order exempting insiders of certain foreign private issuers from Section 16 reporting, please see:

For the SEC’s order, please see:

SEC and CFTC Release Interpretation on Application of Federal Securities Laws to Crypto Assets

On March 17, 2026, the SEC and CFTC issued a joint interpretation clarifying how the federal securities laws apply to certain crypto assets and transactions (the “Interpretation”). The Interpretation does not supersede or replace existing law, but explains the SEC’s views on how the law, specifically the Howey test for determining whether an asset or transaction is a security, applies to these assets and transactions.

The Interpretation classifies crypto assets into five categories based on their characteristics, uses and functions: (i) digital commodities; (ii) digital collectibles; (iii) digital tools; (iv) stablecoins; and (v) digital securities. It clarifies that digital commodities, digital collectibles, digital tools, and certain stablecoins are not themselves securities, but notes that those assets may be offered and sold subject to an investment contract, which itself is a security. Finally, the Interpretation explains that certain crypto asset activities, including “protocol mining” and “protocol staking,” “wrapping” of assets, and “airdrops” disseminating non-security crypto assets, are not subject to the federal securities laws. The Interpretation also states that the CFTC will administer the Commodity Exchange Act consistent with the Interpretation and that certain non-security crypto assets could meet the definition of “commodity” under the Commodity Exchange Act.

Key Takeaways

-

Most forms of crypto assets and activities are not securities. The Interpretation reflects the SEC’s view that “most crypto assets are not themselves securities.” The SEC classifies each type of asset into five categories by assessing how the assets derive their value and whether a purchaser would reasonably expect profits from essential managerial efforts. This “token taxonomy” reflects the SEC’s perspective that four of the five categories of crypto assets are not securities. Moreover, even if a non-security crypto asset is offered or sold subject to an investment contract, which is a security, the underlying crypto asset itself does not become a security.

-

Securities remain securities regardless of format or label. A “tokenized” security, or security that is represented by a crypto asset, does not cease to be a security just because it is offered, sold, and/or represented on the blockchain. In other words, a financial instrument that meets the traditional definition of a security is a security—whether it is represented by a paper certificate, digital token, or otherwise does not affect this analysis.

-

Investment contracts may terminate. When a non-security crypto asset is offered or sold subject to an investment contract under the Howey test, those transactions are subject to federal securities laws. However, the investment contract comes to an end when the representations or promises forming the investment contract are fulfilled, or there is no longer a reasonable expectation that they can or will be fulfilled, at which point subsequent transactions in the underlying non-security crypto asset are not securities transactions.

Practical Implications

SEC Chairman Atkins previewed the token taxonomy and investment contract analysis in November of last year, and the Interpretation issued by the SEC is largely consistent with his earlier comments. While the Interpretation does not change existing, binding precedent such as Howey, it reflects the SEC’s view that most crypto assets are not themselves securities under that analysis. In his March 17, 2026 speech at the D.C. Blockchain Summit, Chairman Atkins reinforced that view, noting that under the Interpretation, only “traditional securities that are tokenized” remain subject to federal securities laws. He also remarked that “a key tenet of our interpretation is that the project team clearly discloses the representations or promises that they make, so investors understand the bundle of rights they are purchasing.” A few days later at SEC Speaks, Chairman Atkins framed the Interpretation as part of the SEC’s broader efforts to clarify the regulatory regime to streamline oversight and unlock innovation. He also said that the Interpretation “amounts to a beginning, not an end” of these efforts.

Crypto asset issuers and developers should take note of the emphasis on explicit, unambiguous, and detailed public disclosures at the time an asset is offered, sold, or issued, at the time any prior representations or promises are fulfilled, or when circumstances change that would render any prior representations or promises no longer applicable. In particular, the Interpretation suggests that the SEC’s view is that where there are no explicit representations or promises made by or on behalf of an issuer in connection with the offer, sale, or issuance of a crypto asset, no investment contract is formed. However, courts addressing this question have taken a more expansive view of when an investment contract is formed, suggesting that there need not be any particular explicit promise by the issuer. Thus, although the Interpretation clarifies the SEC’s view of when crypto assets are securities, we will continue to monitor how courts address this issue moving forward.

For the full text of our memorandum, please see:

For the Interpretation, please see:

Delaware Supreme Court Upholds DGCL 144 Amendments

In Rutledge v. Clearway Energy Group LLC, the Delaware Supreme Court upheld the constitutionality of the 2025 amendments to Section 144 of the Delaware General Corporation Law in a unanimous en banc decision authored by Justice Traynor. The amendments established safe harbor protections from liability for controlling stockholder and other interested transactions that satisfy specified protections, namely approval by a special committee and/or majority-of-the-minority stockholder vote. These amendments provided much needed certainty and a clear roadmap for deal parties to follow. The Delaware Supreme Court’s ruling brings to a close a period of unpredictability surrounding these types of transactions and reflects the ability of the State to respond quickly and in a balanced manner to settle corporate governance and business disputes.

In the opinion, the court stated that legislative acts “‘should not be declared invalid unless [the legislative enactment’s] invalidity is beyond doubt.’” Specifically, the court addressed two questions of law: whether the amendments violated Delaware’s Constitution by (i) divesting the Delaware Court of Chancery of its equitable jurisdiction by eliminating its ability to award equitable relief or damages when the safe harbor provisions are satisfied and (ii) by applying the safe harbors retroactively to fiduciary claims arising from acts and transactions occurring before the amendments’ enactment other than those commenced in any court action or proceeding on or before February 17, 2025. The Supreme Court’s answer to both questions was no. More specifically, it held that the amendments did not eliminate the Court of Chancery’s equitable jurisdiction or extinguish any vested rights unconstitutionally, but rather established a new legal framework for the courts to follow in the future.

For the full text of our memorandum, please see:

For the full text of our previous memorandum concerning the enactment of the 2025 amendments to Section 144 of the Delaware General Corporation Law, please see:

-

https://www.paulweiss.com/media/abmf23eb/significant_delaware_corporation_law_amendments_enacted.pdf

For the Delaware Supreme Court’s en banc decision in Rutledge v. Clearway Energy Group LLC, please see:

Delaware Supreme Court Clarifies Implied Covenant of Good Faith and Fair Dealing

In Johnson & Johnson et al. v. Fortis Advisors, LLC (“Johnson & Johnson”), the Delaware Supreme Court reversed, in part, the Delaware Court of Chancery’s ruling that a buyer breached the implied covenant of good faith and fair dealing (the “implied covenant”) by failing to satisfy its efforts obligations with respect to regulatory approvals needed to achieve an earnout milestone. The opinion clarifies the narrow limits of the implied covenant and reinforces the primacy of the express contractual agreement between parties.

Background

Johnson & Johnson arose in the context of J&J’s acquisition of Auris Health, Inc. The merger included up to $2.35 billion in earnout payments contingent on J&J’s using “commercially reasonable efforts” to achieve regulatory and sales milestones for Auris’s robotic-assisted surgical devices (RASDs). Each regulatory milestone was expressly conditioned on a specific means of U.S. Food & Drug Administration (FDA) regulatory clearance—the “510(k) pathway”—which was the least onerous means of clearance. After closing, a change at the FDA closed the 510(k) pathway for the Auris RASD, and J&J declined to pursue the alternate, more onerous pathway for regulatory clearance—the “De Novo pathway.” No milestones were achieved and thus no earnout payments were made. The plaintiff, a representative of the former Auris stockholders, sued on several theories.

In a post-trial opinion, the Delaware Court of Chancery held that J&J breached the implied covenant by not seeking the De Novo pathway to achieve the first earnout milestone when the 510(k) pathway was closed by the FDA. On appeal, the Delaware Supreme Court reversed that holding, finding that there was no genuine contractual gap for the implied covenant to fill as the merger agreement repeatedly and expressly conditioned the regulatory earnout milestones on the 510(k) pathway and, therefore, allocated to Auris stockholders the risk that regulatory developments might affect the regulatory pathway, timing or cost of approval. Thus, J&J did not breach its obligations to use “commercially reasonable efforts” under the terms of the merger agreement for the first earnout milestone. The Supreme Court affirmed the Court of Chancery’s other holdings, including with respect to breaches of efforts obligations for the other milestones.

Takeaways

The main takeaway from the decision is the court’s clarification of the limited availability of the implied covenant to address contractual claims. The Supreme Court clarified that the implied covenant primarily operates in one of two ways—first, relevant here, as a gap-filling mechanism to address unforeseen developments, and second, not relevant here, when a contract allocates discretionary authority and the court must apply the implied covenant to ensure that discretionary authority is applied consistent with the agreed bargain. As to the first scenario, the court stated that the covenant as gap-filler is a “limited and extraordinary remedy” that only applies when there is a “genuine contractual gap about a truly unanticipated development and only then to vindicate the parties’ shared expectations at signing.” Importantly, the court stressed that a post-closing development sought to be filled by the implied covenant must not only be one that the parties failed to consider, but it must be one that the parties could not have anticipated. If a development, even if unlikely, could have been anticipated, the implied covenant “cannot be invoked to provide protections that ‘easily could have been drafted’ at the bargaining table.” Here, the risk that the FDA would require the De Novo pathway for the first milestone instead of the 510(k) pathway was “both foreseeable and addressed in the parties’ carefully negotiated agreement.” Thus, the opinion reinforces the narrowness of any remedies that can be sought based on the implied covenant if the circumstances are expressly addressed in an agreement.

For the full text of our memorandum, please see:

For the Delaware Court of Chancery’s decision in Johnson & Johnson, please see:

Preparing for M&A Activism in 2026

The resurgence in M&A activity over the past 12 months has greatly increased the likelihood of an uptick in M&A activism in 2026. Recent trends are already showing a growing share of activist campaigns focused on catalyzing transactions, opposing announced deals or reshaping portfolios through break‑ups and divestitures, particularly at companies trading at a valuation discount. Momentum for M&A activism is likely to grow in the coming months, fueled by increasing sponsor buyout activity, a favorable regulatory environment and supportive credit markets. Adding to this momentum is the fact that M&A-driven activism has been at near-term lows: historically, approximately half of all activism campaigns have involved M&A demands, but only about a third of the campaigns in the past three years have involved M&A theses.

M&A Trends Likely to Dominate 2026

In the coming months, we anticipate activists pursuing M&A demands in the following ways:

-

Pushing for a strategic review at companies that are potential buyout targets. Small- and mid-cap public companies with strong cash flow could become targets for activists as private equity sponsors look to deploy dry powder. Companies operating in sectors that have been overlooked by the AI boom but otherwise have strong fundamentals may be particularly attractive given their relative valuation.

-

Teaming up with sponsors to push for a sale. The line between private equity and activists often blurs during periods of robust dealmaking, and the coming months could signal a gradual return of private equity cooperation and teaming up with activists to put companies in play. Activists may also seek to broker deals by identifying potential targets for sponsors.

-

Inserting themselves in strategically transformative transactions. Activists may seek to gain influence within companies rumored to be exploring a potential transaction in order to increase the odds of such a transaction being consummated. Such actions may include seeking access to information or nominating directors to the board.

-

Opposing announced M&A and/or engaging in bumpitrage. Where announced transactions fail to meet market expectations (or in many cases, the activist’s expectations), activists may agitate against the transaction, or alternatively, urge the parties to revise the transaction terms in order to make a quick and outsized return.

-

Pushing for break-ups and divestitures. Portfolio simplification will likely continue to be a priority for activists, as investors reward focused portfolios and easily understandable strategies. We expect companies with disparate or underperforming segments to continue to face activist pressure to simplify their operations through M&A.

The Unique Challenges of Managing M&A Activism

Preparing for and responding to M&A activism can be uniquely challenging. Unlike activist campaigns centered around operational, capital allocation or governance demands, boards and management face greater legal constraints and heightened market scrutiny when engaging in conversations, public or private, relating to M&A. When faced with an activist making M&A-related demands, management teams and boards would be well advised to consider the following:

-

Recognize that maintaining confidentiality is essential. While keeping discussions with an activist private can be advantageous across all activism situations, maintaining confidentiality is critical in M&A-oriented campaigns where leaks and rumors about an activist campaign can disrupt a sale process or inadvertently put a company in play. Knowing when and how to engage with an activist and whether and when to bring an activist under the tent are among the key tactical decisions targeted companies will need to make.

-

Be prepared to respond under a compressed timeline. M&A activism can create potentially irreversible market signaling effects that do not exist in other types of activist campaigns. Public discussion of a sale may reshape expectations among investors, employees, customers and business partners, and if not promptly addressed can create the expectation of an M&A transaction. And once an M&A thesis gains traction, the board and management may face an uphill battle persuading investors to support other value creation pathways.

-

Understand that governance processes and board records will be scrutinized. Governance issues are often the focal point of an M&A activism campaign because a flawed (or failed) sale process can help an activist discredit the board and management and provide the basis to terminate or revise an announced transaction, re-evaluate proposals that have been rejected by the board or commence a new sale process. Consequently, how a sale process is structured and how board deliberations are documented are important issues to consider when preparing for M&A activism.

-

Expect subsequent annual meetings to become a referendum on an announced transaction. The decision of shareholders to remove three James Hardie directors following the company’s poorly received acquisition of AZEK last year underscores how annual meetings can become a shareholder referendum on the transaction even when a shareholder vote is not required to approve the transaction. Activist shareholders may also look to capitalize on investor frustration by running a vote-no campaign against directors.

-

Response strategies will need to evolve. M&A activism often focuses attention on whether the board and management have adequately tested a company’s strategic alternatives. In this context, partial concessions, reaffirmations of conviction in long-term strategy and incremental governance improvements can be ineffectual if the board has not delivered a credible response.

M&A activism activity is likely to increase in 2026. For boards and management teams, the key risk is being unprepared for how quickly an M&A-oriented campaign can narrow strategic discretion, compress timelines and reshape shareholder expectations. In this environment, early preparation, disciplined governance processes and a clear understanding of when and how to engage are essential to preserving optionality and maintaining control of outcomes when M&A activism surfaces.

For the full text of our memorandum, please see:

Five Ways AI Could Transform Coming Proxy Seasons

Recent decisions by J.P. Morgan Asset Management and Wells Fargo to deploy artificial intelligence (“AI”) to guide proxy voting are evidence of deeper structural changes already underway that could transform future proxy seasons. The near-term impact of AI will likely be most acutely felt in the shift away from benchmark voting policies developed by proxy advisors to customized voting policies developed with the aid of AI. Over the medium to longer term, AI could potentially upend the tactics, tools and timing of future proxy contests. We highlight below five potential changes that could occur in the coming years.

1. What Gets Measured May Matter More Than What Gets Said

As AI tools increasingly inform voting decisions, how AI algorithms are constructed, trained and calibrated could determine the outcome of proxy contests. To date, solicitation efforts have centered around human decision makers at proxy advisors and institutional investors, who have in turn largely relied on materials shared by the company and activist. But as AI empowers institutional investors to independently gather and analyze information with increasing efficiency and accuracy, the relative influence of fight decks and fight letters—which have been the central components of a proxy contest—could diminish, along with traditional proxy solicitation strategies focused on disseminating such materials.

What may matter more in future proxy contests is convincing investors of what issues, metrics and trends deserve the greatest attention. Engagement efforts may need to focus on inputs—data sources, weighting methodologies and interpretive assumptions—rather than on specific outcomes. Adopting a “kitchen sink approach” to fighting proxy contests may also become less credible as the growing availability of data and analysis will more easily expose weaker arguments.

2. One Investor, Multiple Vote Outcomes

AI tools may allow institutional investors to develop more granular policies tailored to specific funds and designed to address a greater range of topics and metrics. By contrast, today’s proxy voting policies at most institutional investors are applied across funds. This shift could be particularly pronounced among actively managed funds, who may face greater pressure to further tailor their voting practices to specific fund mandates. Passive investors, who continue to face regulatory pressure to remain “passive,” may also deploy AI tools to facilitate more surgical approaches to proxy voting.

Over time, voting outcomes could diverge more sharply across funds managed by the same institutional investor. For issuers and activists alike, this could mean fewer predictable “house votes.” Proxy contests may become less about persuading institutional investors as a whole and more about identifying and targeting the most consequential funds.

3. Speed and Intensity of Proxy Contests Accelerate

Artificial intelligence may accelerate the speed and intensity at which proxy contests are fought. AI’s potential to capture, analyze and react to public disclosures in near real-time could compress timelines for response and place a premium on proactive and preemptive messaging and rapid correction of the record before new information begins to influence voting outcomes. AI tools may also make it easier for companies and activists to increase the volume and cadence of messaging to investors and tailor their messaging and engagement strategies to fund-specific mandates and voting patterns, which may in turn further accelerate the intensity of proxy contests. Investor sentiment could also shift meaningfully during the course of a proxy contest as AI tools enhance information availability. Consequently, vote predictions may become more difficult, and settlement discussions (which are primarily driven by the leverage wielded by each side) could also become less predictable and more complex.

4. Lower Barriers to Entry Increase Activist Activity

AI will likely lower the barrier to entry for activist investing. AI‑enabled screening tools can help reduce the cost and time required to identify potential targets, develop campaign theses and execute campaigns. Consequently, a broader set of activists, including new entrants and occasional participants, may pursue campaigns that would not have been economically practicable in the past. Given that there is a finite number of attractive targets at any given time, an increase in the number of activists could lead to increased swarming behavior and multi-year and off-cycle activity as multiple activists seek to gain credibility, visibility, and traction around similar themes or targets. In this new environment, the quality, originality and persuasiveness of ideas may matter more than ever.

5. Cadence and Frequency of Shareholder Engagement May Shift

AI could reshape when investors choose to engage with companies and continue to blur the lines between “off” and “in-season” engagement. Institutional investors are already deploying AI tools to evaluate public disclosures, identify engagement priorities and targets and inform engagement agendas. AI is being used to review proxy statements, quarterly and annual reports, earnings materials and peer data across time to identify emerging risks or material changes in a company’s operations, strategy and governance. The availability of such data may allow the largest passive funds to become even more targeted in their engagement efforts, particularly as changes to the SEC’s guidance on Schedule 13G filing eligibility has continued to dampen index fund appetite for engagement. For active investors, the deployment of AI systems to continuously ingest information could encourage more spontaneous engagements driven by new disclosures and market developments.

Looking Ahead

The growing use of artificial intelligence in proxy voting signals a likely shift in how future proxy seasons may unfold. Future proxy contests are likely to become more data‑driven, faster‑moving, and more competitive. The adoption of AI may reduce the influence of traditional solicitation tools, reduce the transparency of voting policies, lower barriers to entry for activism and alter the cadence and nature of shareholder engagement. Going forward, companies and activists alike will need to adapt their strategies to a proxy voting landscape that is increasingly shaped by algorithms, analytics and real‑time information flow.

For the full text of our memorandum, please see:

HSR Notification Requirements Revert to “Old” Rules

As the result of a single-sentence order by the United States Court of Appeals for the Fifth Circuit on March 19, 2026, the pre‑February 2025 Hart-Scott-Rodino (“HSR”) Act notification requirements have been reinstated, effective immediately.

The HSR Act requires that mergers and acquisitions meeting certain monetary thresholds must be notified to the Federal Trade Commission (“FTC”) and Department of Justice (“DOJ”) Antitrust Division prior to closing. In February 2025, the FTC implemented major changes to the HSR Act Rules (including the HSR Form required under the Rules). These changes imposed significantly greater burden and expense on filing parties. On February 26, 2026, in a challenge by the Chamber of Commerce to the FTC’s rule making, a federal district court in Texas set aside and vacated the February 2025 revisions to the HSR Act reporting requirements.

On March 19, 2026, a three-judge panel of the Fifth Circuit—consisting of two judges appointed by Democratic presidents and one judge appointed by a Republican president—denied the FTC’s motion to stay the district court decision until resolution of the FTC’s appeal. The Fifth Circuit summarily stated “that Appellants’ opposed motion for stay pending appeal is DENIED.”

With these thirteen words, the new HSR Rules that went into effect February 10, 2025 and placed a significantly higher up‑front burden and expense on filers no longer govern the HSR Act notification requirements. Instead, filing parties may now use the less burdensome, pre-February 2025 HSR Rules and form. Some of the information that filers will no longer need to provide is:

-

The identification of a Supervisory Deal Team Lead in connection with producing transaction-related competitive analyses;

-

A list of officers and directors who serve in similar capacities at other companies in the same industry as the target;

-

Ordinary course CEO and board plans and reports;

-

Narrative descriptions of competitive and supply relationships (i.e., sales and purchases) between the parties and their competitors;

-

Lists of ex-U.S. competition act filings and filings with state attorneys general;

-

Detail regarding foreign subsidies, countervailing duties and investigations, and defense contracts.

While the reversion to the pre-February 2025 Form will significantly reduce the disclosures, filers will now need to collect detailed manufacturing revenue figures by NAPCS code and NAICS revenue figures (instead of ranges) to complete the old Form. No other incremental information will be required. The change may also result in shorter time frames to make HSR Filings after signing.

Notably, the Fifth Circuit’s March 19 order addressed only the FTC’s motion to stay and it has yet to rule on the merits of the FTC’s appeal. The FTC’s appeal to the Fifth Circuit of the district court’s order is still ongoing and a decision could take months.

For the full text of our memorandum, please see:

For the full text of our previous memorandum concerning the changes to the HSR Act Rules, please see:

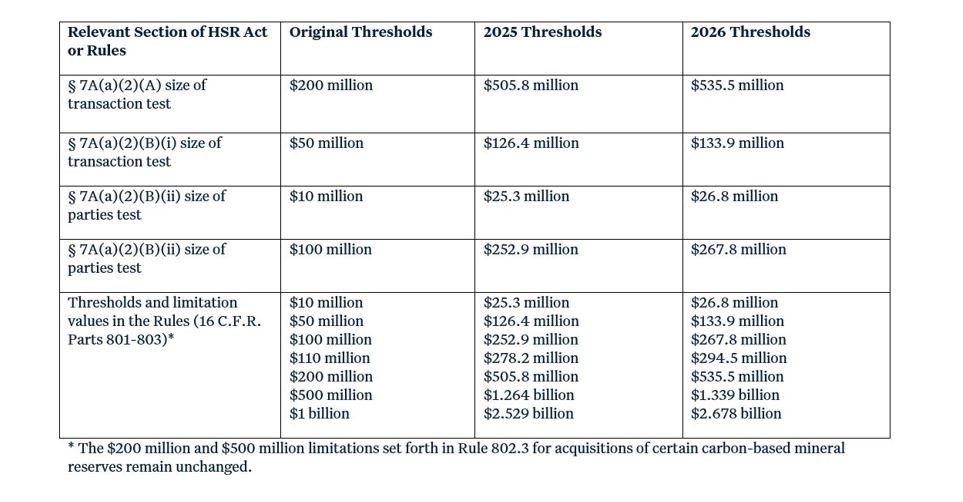

Hart-Scott-Rodino and Clayton Act Section 8 Thresholds for 2026

The Federal Trade Commission (FTC) has revised the jurisdictional and filing fee thresholds of the Hart-Scott-Rodino Antitrust Improvements Act of 1976 (HSR Act) and the Premerger Notification Rules, based on changes in the gross national product (GNP) as required by the 2000 amendments to the HSR Act. The filing thresholds and fees increased as a result of the increase in the GNP and apply to transactions that closed on or after February 17, 2026. These threshold and filing fee adjustments occur annually and do not alter the HSR filing process.

The HSR Act requires parties intending to merge or to acquire assets, voting securities or certain non-corporate interests to notify the FTC and the Department of Justice, Antitrust Division, and to observe certain waiting periods before consummating the acquisition. Notification and Report Forms must be submitted by the parties to a transaction if both the (1) size of transaction and (2) size of parties thresholds are met, unless an exemption applies.

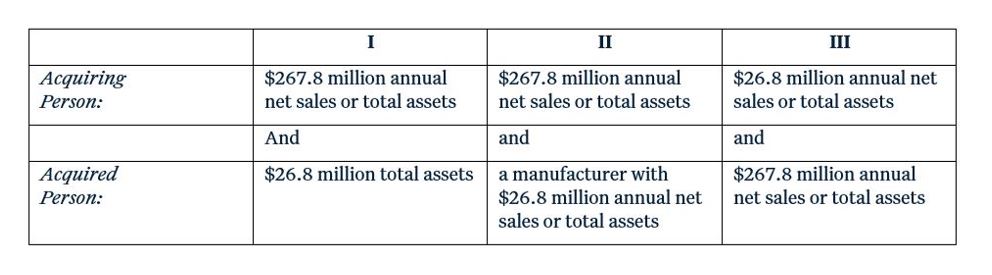

Size of Transaction

The minimum size of transaction threshold is $133.9 million, increased from the 2025 threshold of $126.4 million.

Size of Parties

The size of parties threshold is inapplicable if the value of the transaction exceeds $535.5 million ($505.8 million in 2025). For transactions with a value between $133.9 million and $535.5 million, the size of parties threshold must be met and will be satisfied in one of the following three ways:

|

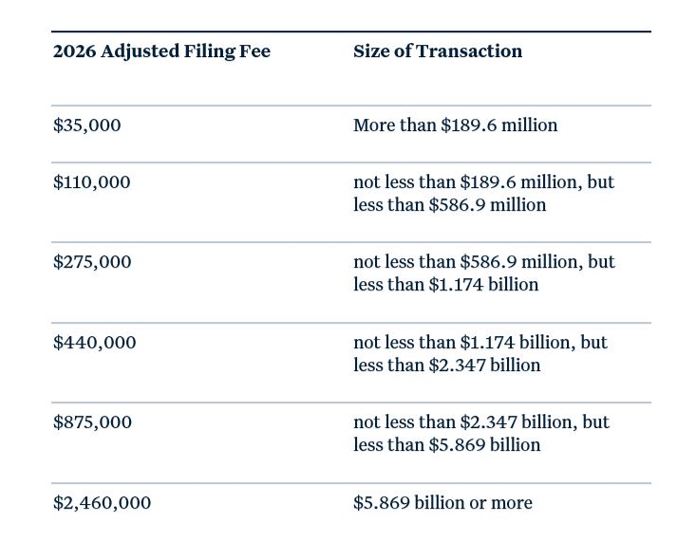

The various jurisdictional thresholds, notification thresholds, filing fee thresholds and thresholds applicable to certain exemptions will also increase, as illustrated below.

|

|

The above thresholds and fees will continue to adjust annually. The current maximum civil penalty for HSR Act violations is $53,088 per day, which is expected to increase soon.

Section 8 Interlocking Directorate Thresholds

Finally, the FTC has increased, effective as of January 16, 2026, the thresholds that prohibit, with certain exceptions, competitor companies from having interlocking relationships among their directors or officers under Section 8 of the Clayton Act. Section 8 provides that no person shall, at the same time, serve as a director or officer in any two corporations that are competitors, such that elimination of competition by agreement between them would constitute a violation of the antitrust laws. There are several “safe harbors” which render the prohibition inapplicable under certain circumstances, such as when the size of the corporations, or the size and degree of competitive sales between them, are below certain dollar thresholds. Competitor corporations are now subject to Section 8 if each one has capital, surplus and undivided profits aggregating more than $54,402,000, although no corporation is covered if the competitive sales of either corporation are less than $5,440,200. Even when the dollar thresholds are exceeded, other exceptions preventing the applicability of Section 8 may be available. In particular, if the competitive sales of either corporation are less than 2% of that corporation’s total sales, or less than 4% of each corporation’s total sales, the interlock is exempt. In addition, Section 8 provides a one-year grace period for an individual to resolve an interlock issue that arises as a result of an intervening event, such as a change in the capital, surplus and undivided profits or entry into new markets.

For the full text of our memorandum, please see:

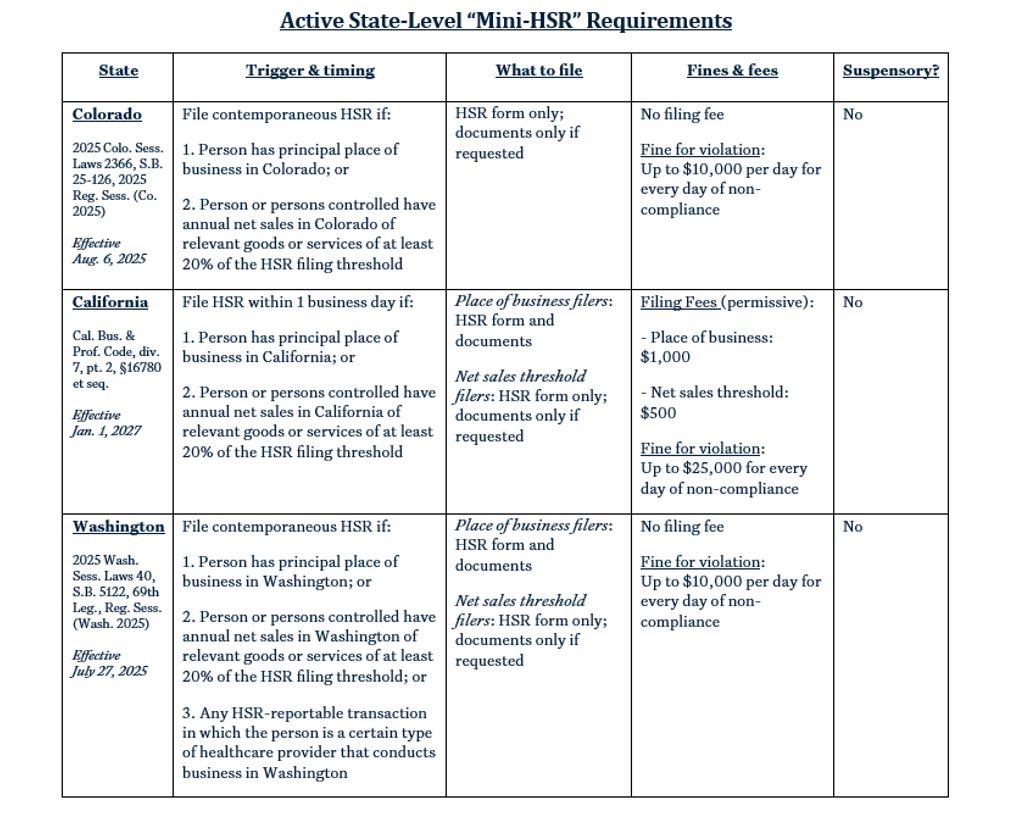

California Enacts Mini-HSR Law

California joins Washington and Colorado in adopting a state-level “mini-HSR” law, with bills pending in a half dozen other states. Below is a summary of the active state-level “mini-HSR” requirements:

|

Takeaways

-

Driven by state-level antitrust enforcement efforts, states are increasingly requiring “mini-HSR” notices for certain transactions. In 2025, Washington and Colorado enacted such laws, and late yesterday, California followed with its own law. There are also similar bills pending in New York, the District of Columbia, Hawaii, Indiana, and West Virginia. These bills come at a time where we are seeing state attorneys general pursue antitrust enforcement even where they depart from federal enforcement decisions.

-

Critically, so far, these are notice-only filings and, unlike HSR, do not impose their own waiting periods. The bills do differ somewhat in that some, but not all, require production of deal-related documents. California also adds modest fees to its requirement.

What deals are affected?

On February 10, 2026, California Governor Gavin Newsom signed into law SB 25, California’s version of the Uniform Antitrust Premerger Notification Act (“UAPNA”), which requires certain merging parties to notify their transactions to state authorities. Beginning January 1, 2027, California will require the following categories of persons making an HSR filing also to file a copy with the California Attorney General (“AG”):

-

a person that has its principal place of business in California; or

-

a person, or a person it directly or indirectly controls, had annual net sales in California of at least $26.78 million of the goods or services involved in the transaction.

Principal place of business filers must submit to the AG any additional documentary materials filed under the HSR Act, while size of transaction threshold filers must only do so at the request of the AG. The AG may impose a filing fee of $1,000 for the former or $500 for the latter, with both filers subject to a potential civil penalty of $25,000 per day of noncompliance.

Submissions (including the fact of the submission and the proposed merger) must be kept confidential by the AG and are protected from disclosure, though the AG can share the submission with attorneys general of other states with a substantially similar law. Unlike the federal HSR law, the act does not impose a waiting period that parties must observe before closing.

Versions of the UAPNA have already been enacted in Washington and Colorado; and others have been introduced in the District of Columbia, Hawaii, Indiana, and West Virginia. A broader antitrust bill that includes premerger notification requirements is pending in the New York legislature. Still other states have premerger notification requirements limited to certain healthcare transactions, whereas the uniform act is broadly applicable.

For the full text of our memorandum, please see:

For the full text of SB 25, please see:

DOJ Files First-Ever Complaint to Enforce Presidential Divestment Order in CFIUS Matter

On February 9, 2026, the DOJ took unprecedented action by filing a complaint under Section 721 of the Defense Production Act of 1950 to enforce President Trump’s July 8, 2025, Executive Order “Regarding the Acquisition of Jupiter Systems, LLC by Suirui International Co., Limited.” This Order barred Suirui Group Co., Ltd. (“Suirui”)—a Chinese firm—from acquiring Jupiter Systems, Inc. (“Jupiter”), a California-based provider of video communications hardware and software, and demanded that Suirui divest all interests in Jupiter. The DOJ’s move marks the first time the federal government has sought judicial enforcement of a presidential divestment order recommended by the Committee on Foreign Investment in the United States (“CFIUS”).

The enforcement action underscores the U.S. government’s willingness to pursue all available remedies when parties fail to comply with CFIUS-mandated divestment orders and signals continued aggressive enforcement of national security-related investment restrictions, particularly involving Chinese investors in U.S. technology companies.

Background

In 2020, Suirui Group, through its Hong Kong subsidiary Suirui International Co., Limited, acquired all of Jupiter Systems, which provides video communications hardware and software to commercial and U.S. Government customers. After the transaction closed, CFIUS identified a national security risk arising from Suirui’s ownership of Jupiter relating to the potential compromise of Jupiter’s products used in military and critical infrastructure environments.

On July 8, 2025, the Trump Administration issued an Executive Order prohibiting the transaction based on his finding that the transaction posed a threat to national security. The Order required Suirui to divest all its interests in Jupiter within 120 days (subject to extension by CFIUS) and imposed immediate restrictions on access to Jupiter’s non-public source code, technical information, IT systems, and U.S. facilities.

On February 9, 2026, after CFIUS granted two extensions of the divestment deadline, the DOJ filed a lawsuit in the U.S. District Court for the District of Columbia to enforce the divestment order.

Key Takeaways and Practical Implications

-

First judicial enforcement of a CFIUS divestment order. This complaint represents the first time the Department of Justice has filed a lawsuit in federal district court to enforce a presidential order requiring divestiture under Section 721 of the Defense Production Act. The action demonstrates that the government will pursue litigation when parties fail to comply with divestment mandates. Enforcement actions under the Defense Production Act are exceptionally rare, likely because companies typically comply with divestment orders; therefore, this case stands out not only for the government’s decision to litigate but also for the unusual instance of corporate noncompliance.

-

Enforcement of orders involving non-notified transactions. The Suirui-Jupiter transaction closed in 2020, more than five years before the President issued the divestment order. This timeline underscores that CFIUS continues to actively identify and act on transactions subject to CFIUS jurisdiction for which no voluntary notice or declaration was filed with CFIUS.

-

Continued focus on Chinese investment in U.S. technology. The action aligns with the U.S. government’s policy efforts to restrict investments by Chinese persons and companies in sensitive U.S. sectors. Companies engaged in cross-border M&A involving U.S. technology assets should carefully assess CFIUS risk and consider the implications of non-notified inquiries, including the possibility of post-closing divestment orders and related compliance obligations.

-

Potential consequences of non-compliance. The lawsuit makes clear that failure to comply with CFIUS-mandated divestment orders may result in federal court enforcement actions. CFIUS also has the power to impose monetary penalties for non-compliance with divestment terms, mitigation agreements, and other conditions.

-

The U.S. government will pursue all available remedies to enforce CFIUS divestment orders. The DOJ’s lawsuit represents a novel approach by the U.S. government in enforcing a CFIUS divestment order, reflecting the U.S. government’s prioritization of foreign direct investment laws as an enforcement priority.

-

CFIUS enforcement actions can be initiated years after closing. The transaction underlying the complaint closed in 2020, underscoring that CFIUS continues to identify and act on non-notified transactions, even years after closing.

For the full text of our memorandum, please see:

For the full text of our prior memorandum concerning the July 8, 2025 Executive Order, please see:

For the full text of the DOJ’s complaint in United States v. Suirui Group Co., Ltd, please see:

* * *